Greenlight Debit Card Alternatives will be discussed in this article. If you’re thinking about getting your child a debit card, you might be wondering what your options are. The Greenlight debit card, for example, is one of the most popular options for teaching youngsters how to earn, save, provide, and invest. Although Greenlight is a popular option for many parents looking for children’s debit cards, you do have alternative options. Many Greenlight debit card alternatives provide many of the same features, if not all of them.

10 Best Greenlight Debit Card Alternatives In 2022

You may learn about Greenlight debit card alternatives in this article; here are the details:

We’ve found the best Greenlight Debit Card Alternatives to assist you in teaching your children good money management practises that will help them succeed financially.

When it comes to children’s debit cards, you’ll want to choose one that meets your family’s needs and budget.

The finest Greenlight Debit Card Alternatives are listed below in order of preference.

1. Acorns Family

Acorns are well known for its adult accounts, which allow you to acquire fractional shares of stock with roundups from associated debit and credit card purchases.

You can open an Acorns bank account and use your Acorns debit card to make purchases. This just costs $3 per month.

What you may not realize is that Acorns Family caters to families with children. You get financial investing accounts for unrestricted kids when you open an Acorns Household account for $5 per month.

Even better, this account includes retirement, investment, and inspection accounts, as well as bonus offer investments, financial advice, and much more.

Keep in mind that there is no straightforward debit card for your child with Acorns. However, you can give your youngster the ability to make purchases by opening an Acorns bank account in your name.

However, you must accompany your children when they make purchases.

Rate: $5 monthly.

Advantages – There are six ETF portfolios to choose from.

– Make investments for both adults and children.

— Reasonable monthly fee

Disadvantages- There is no dedicated debit card for children.

– There is no option for a financial investment account for education.

2. Axosbank

The Axos First Bank account is for children aged 13 to 17. Account owners who are teenagers should have a dual adult account owner.

The account comes with a complimentary debit card that is fee-free when used at in-network ATMs. You can also get up to $12 in monthly ATM fee rebates.

The Axos First Bank account also has the following features:

-There is no requirement for a minimum balance.

-$50 as a minimum first deposit

-$0 in monthly service fees

-A daily ATM limit of $100/a daily purchasing limit of $500

— Notifications of activities in real-time

— It bears interest.

Using the app or the website, parents can control who has access to their debit cards. Axos’ recommendation program allows kids to make peer-to-peer transfers.

This account also includes biometric recognition and bill payment. For additional information, see the Axos website.

Each month, there is no charge.

Advantages. – This is an interest-bearing account.

– A wide range of parental restrictions.

– There are no overdraft fees.

Disadvantages: Only a small portion of ATM fees is reimbursed.

– Debit cards have lower limits than other cards.

3. BusyKid.

BusyKid is a prepaid investment card that let your children earn money by doing tasks.

You can utilize the app to designate preset chore selections as a mom or dad. Your child’s money is safe and can be invested everywhere Visa is accepted.

You can also work with your child to put the money in a savings account, invest it in stocks, or donate it to a good organization.

Other features include:

— A parent-directed benefits alternative.

– Family and friends can send money to the account using a QR code.

– Savings pods with a parental match feature.

— Access for many parents.

Your BusyKid account can hold up to 5 children. Keep in mind that each denied purchase will cost you $0.50. (due to insufficient funds).

It’s also vital to remember that each replacement card will cost $7.99.

You can load money onto the card, which can then be used everywhere a Visa debit card is accepted. You can also transfer funds from the card when necessary. Also check : Best Microsoft Project alternatives online 2022

Monthly cost: $3.98+ or $38.99 per year.

Pros. – Affordable price options.

– Accounts can be funded by friends and family.

– Parental control options that are comprehensive.

Cons: There is a significant card replacement price.

4. Chase First Banking.

Teenagers ages 6 to 17 can open a Chase First Banking account. This account has a task app as well as a savings feature. It is highly recommended among Greenlight Debit Card Alternatives.

Moms and dads can choose how much and where a child can invest per transaction. You could, for example, impose a $10 cap on dining places or a $20 limit across the board.

Among the other features are:

-There is no regular monthly payment of $ 0

-$0 is the minimum first deposit.

– Cash withdrawals at Chase ATMs are free.

— Spending in real-time informs.

Children can even request money transfers using the app, which parents can accept or reject.

In order for your child to have a Chase First Banking account, you, as the parents, must have or open a Chase checking account.

Per parent or guardian, approximately 5 Chase First Banking accounts are enabled.

The cost is $0 each month.

Pros :

– Create a chores list and/or set up automatic allowances.

– Ample adult controls that can be adjusted.

– There are no fees.

Cons. – Both the parents and the children must have a Chase account.

– There is no option for a direct deposit.

5. Copper Teenager Banking.

Copper Banking is a fintech company that offers adult accounts. Each adult account holder, however, can have up to five Copper Teen accounts.

Money can be transferred from your bank account or debit card to your Copper account. After then, you can transfer funds to any Copper Teen account.

The following are some of the other Copper Banking functions:

-There is no requirement for a minimum balance.

– Automated payment of allowances.

– The ability to make direct deposits.

– Resources for financial education.

— A function that allows you to set savings objectives.

Copper may only be used by your adolescent if they have their own phone. For some parents, this may be a disadvantage.

Monthly cost: $0

Pros :

– There are no account fees.

– A large network of fee-free ATMs.

– One adult account can be used to create up to five teen accounts.

Cons :

Adult controls are minimal.

– Teens must have access to a cell phone.

6. Existing.

The present is a fintech financial software designed to help children and teenagers learn about earning, spending, saving, and giving.

You can add a teen account for your child when you open a bank account. Existing charges $36 per year for teen accounts.

You have control over transfers to the account as the parent. You can also establish spending limits and ATM withdrawal limits.

There are also the following features:

-There is no obligation for an initial deposit.

-$ 0 minimum balance.

— Fee-free ATM withdrawals within the network.

– The ability to create a task list.

— One cost-cutting pod

– One pod that provides.

Offering pods allow your adolescent to donate money to a charity of their choice. You can give your child weekly allowances, make one-time transfers, or help them with chores on the chore list.

The cost is $36 per year.

Pros.

– A free account for parents is offered.

– Parental restrictions that are both flexible and suitable.

– Direct Deposit is a convenient option.

Cons.

– There is a yearly cost.

– Only one guardian is permitted.

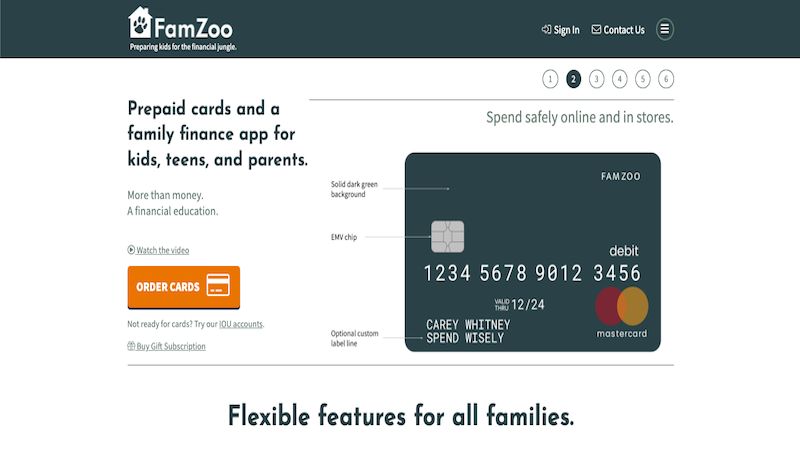

7. FamZoo.

FamZoo is a home financial fintech that was created to help you teach your children about money. An IOU account or a pre-paid account are the two sorts of accounts available.

A pre-paid account, whether it’s for spending, saving, or gifting, holds real money. You’ll use IOU accounts to keep track of the money you owe your child.

You can use IOU accounts, pre-paid accounts, or a combination of the two. In addition, you may use the app to create daily and weekly tasks.

Kids earn money (or you give them a weekly allowance), and then they collaborate with you on how to invest, save, and give it away.

FamZoo also has the following features:

– Complete parental control

– Activity enlightens.

– An alternative is to have the interest paid by the parents.

– The power to add incentives or fees.

For parents who want to praise their children for going above and above or punish them for not following the rules, the perks and charges option is a nice addition.

Keep in mind that paying semi-annually, annually, or bi-annually can save you money in the long run.

The monthly fee is $5.99.

Pros. – Extensive mentorship tools.

— Functions for rewards and penalties.

– Parental controls and functions that are flexible.

Cons – There isn’t a complimentary choice.

– The learning curve is a little steep.

Check also : How To Download Online Videos From Savefrom.net Complete Guide

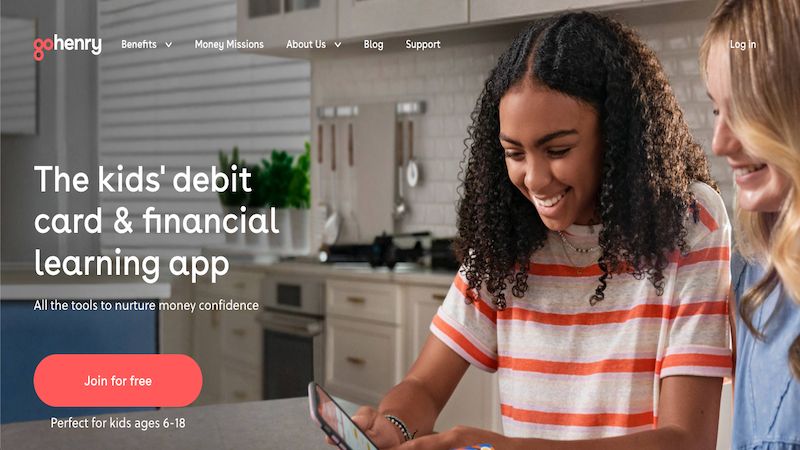

8. GoHenry.

GoHenry is a fintech banking app for kids aged 6 to 17 that includes a debit card. You can create weekly allowances and/or task lists with GoHenry. it is one of the best among Greenlight Debit Card Alternatives.

Your child’s earnings can be kept in a spending account, transferred to savings, or donated to Boys & Girls Clubs of America.

The GoHenry debit card includes the following features:

-$ 0 minimum balance.

• Spending notifications in real-time.

– Spending limits for adults.

– The ability to make direct deposits.

It’s worth noting that GoHenry includes a comprehensive learning centre that’s great for giving kids a better grasp of money. The learning center offers free classes.

Teens can also send and receive money from other GoHenry users. If your kid wants to split a lunch bill or another expense with a friend, this is a fantastic feature to have.

Keep in mind that with GoHenry, your teen will not be able to use the “pay at the pump” feature. They can, however, spend their money at the gas station.

The cost is $3.99 per month.

Advantages. – Comprehensive information center.

— Recommendation-based incentive program.

Cons: There are no complimentary options.

– Debit card costs are subject to additional limits.

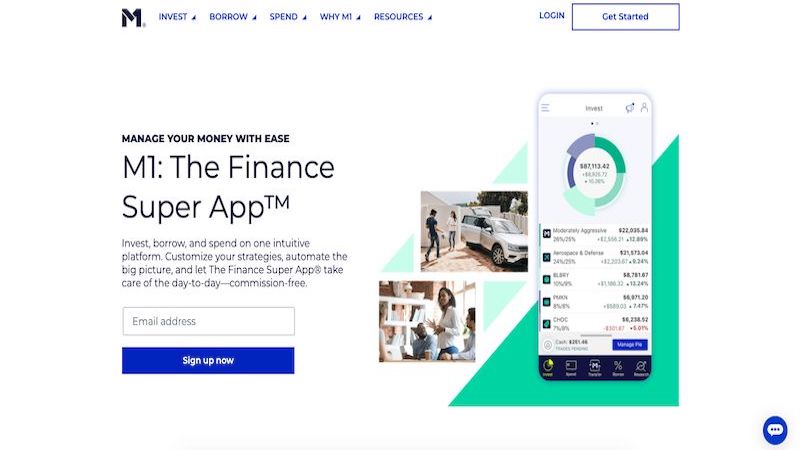

9. M1 Financing.

M1 Finance is a fintech firm that enables adults to spend, save, acquire, and invest. You can open a UTMA/UGMA custodial account for your child with M1 Finance.

The company offers a free regular account. However, in order to create a representative for your child, you must first open a Plus account, which costs $125 per year.

If you use the debit card feature to invest some of the money from the custodial account, you must use the money for the minor child’s direct benefit.

Once the child reaches legal age, the money will be transferred to their ownership. This changes depending on where you reside.

Choosing M1 Financing over other methods has the advantage of allowing you to acquire fractional shares of stocks and ETFs for your child.

There are also the following features:

– Purchases made with a debit card earn 1% cashback.

– Around four regular monthly ATM charge repayments

-A minimum account balance of $ 0 is required.

– There are no fees for debit purchases made anywhere in the world.

M1 Financing is designed specifically for parents who want to spend money on their children’s behalf. The debit card serves as a backup.

You can either build your own portfolio or choose one of M1 Financing’s pre-made portfolios.

The cost is $125 per year.

Pros – Attractive financial investment capabilities.

– Plus members get money back on debit purchases.

– UTMA/UGMA custodial accounts are widely available.

Cons. – Expensive yearly fee (relatively).

– Not specifically designed for children.

10. Mazoola.

Mazoola is a digital wallet for families that may be used to compensate children for tasks. You may now assist them in managing their money, whether it’s saving, spending, or making financial objectives.

Mazoola has the following features:

– Parents and guardians can establish dollar limits and allow merchants.

-$ 0 minimum balance.

– Tasks are a useful feature.

– There is a goal feature.

– Another option is to make charitable gifts.

— Notifications of action in real-time.

Mazoola offers a one-year free trial, despite the subscription rate being a little on the high side.

The monthly fee is $9.99.

Advantages. – Adequate adult controls.

-“Stealable” tasks

— Compatible with Apple Pay and Google Pay.

Disadvantages: There are no real debit cards available.

– Additional fees that aren’t shown on the website.

Summary.

As a teenager, the finest Greenlight options will assist your child in learning to save, invest, and also find ways to generate revenue. That way, when it’s time for them to leave the nest, they’ll be ready.

Take the time to figure out which functions are most important to you. Then, compare the features and costs of each option to see whether Greenlight or another card is the best fit for you.

Also : Clipboard Manipulations : Sorry, No Manipulations With Clipboard Allowed – Solved

![Canvas Lamar Cisd Login at Www.Lcisd.Org Portal – Complete Guide [2022]](https://www.gadgetsmagazine.org/wp-content/uploads/2022/07/canvas-lamar-cisd-login-at-www.lcisd_.org_.png)